Even the Most Sophisticated Investors Aren’t Likely to Outperform

It has been well documented by the annual SPIVA reports that retail mutual funds underperform with great persistence, with any persistence not significantly greater than would be randomly expected. With that said, it seems logical to believe that if anyone could beat the market, it would be the equity mutual funds/ETFs and separately managed accounts (SMAs) of institutional investors (such as pension plans and endowments). Why is this a good assumption? First, these institutional funds control large sums of money. They have access to the best and brightest portfolio managers, each clamoring to manage the billions (or tens of billions) of dollars in these accounts (and earn large fees). Institutional investors can also invest with managers that most individuals don’t have access to because they don’t have sufficient assets to meet the minimums of these superstar managers.

Second, it is not even remotely possible that these institutional investors would ever have hired a manager who did not have a track record of outperforming their benchmarks, or at the very least matching them. Certainly, they would never hire a manager with a record of underperformance.

Third, it is also safe to say that they never hired a manager who did not make a great presentation, explaining why the manager had succeeded, and why she would continue to succeed. Surely the case presented was a convincing one.

Fourth, many, if not the majority, of these institutional investors hire professional consultants such as Frank Russell, SEI, and Goldman Sachs, to help them perform due diligence in interviewing, screening, and ultimately selecting the very best of the best. And you can be confident that these consultants have thought of every conceivable screen to find the best fund managers. Surely, they have considered not only performance records, but also such factors as management tenure, depth of staff, consistency of performance (to make sure that a long-term record is not the result of one or two lucky years), performance in bear markets, consistency of implementation of strategy, turnover, costs, etc. It is unlikely that there is something that you or your financial advisor would think of that they had not already considered.

Fifth, as individuals, it is rare that we would have the luxury of being able to personally interview money managers and perform as thorough a due diligence as do these consultants. And we generally do not have professionals helping us to avoid mistakes in the process.

Sixth, the fees they pay for active management are typically lower than the fees individual investors pay.

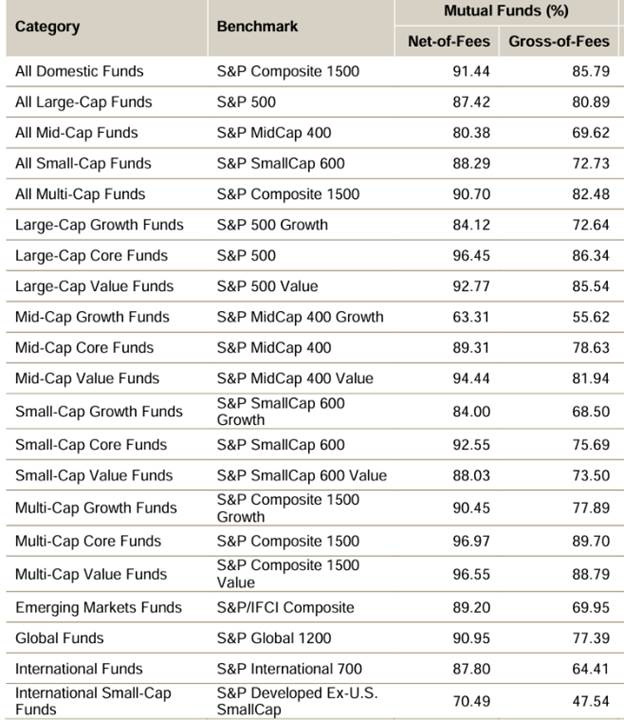

So, how have the institutional funds performed in quest for outperformance? The SPIVA Institutional Scorecard Year-End 2023 sought to answer that question. Their data covers the 10-year period ending December 2023. Here is a summary of their key findings:

The majority of active retail U.S. equity mutual funds underperformed their benchmarks over the 10-year period, even before accounting for fees. Underperformance included those areas that are perceived to be more suited to active management, such as emerging markets and international small-cap funds.

Percentage of Retail Mutual Funds Underperforming over 10 Years

Relative to retail equity mutual funds, institutional equity fund provided superior performance as “just” 81% of them underperformed versus 89%.

Institutional SMAs/Wrap Accounts performed even worse as 95% of them underperformed.

Percentage of U.S. Equity SMA/Wrap Managers Underperforming over 10 Years

Confirming Evidence

SPIVA’s findings are consistent with those found by Richard Ennis in his 2020 study “Institutional Investment Strategy and Manager Choice: A Critique.” Richard Ennis found that institutional investors underperformed. For example, he found that public pension plans underperformed their benchmark return by 0.99% and endowments underperformed by 1.59%. He also found that of the 46 public pension plans he studied, just one generated statistically significant alpha, compared to the 17 that generated statistically significant negative alphas. He calculated that “the likelihood of underperforming over a decade is 0.98—a virtual certainty.”

SPIVA’s findings are also consistent with the empirical findings on the performance of pension plans.

Performance of Pension Plans

The 2005 study, “The Selection and Termination of Investment Management Firms by Plan Sponsors,” provides further evidence on the inability of plan sponsors to identify investment management firms that will outperform the market post-hiring. The authors examined the selection and termination of investment management firms by plan sponsors. The database covered approximately 3,700 plan sponsors from 1994 to 2003. Here are their key findings:

• Plan sponsors hired investment managers after large positive excess returns up to three years prior to hiring.

• Post-hiring excess returns were indistinguishable from zero.

• If plan sponsors had stayed with the fired investment managers, their returns would have improved—all the activity was counterproductive.

The 2000 study, “A Panel Study of Equity Pension Fund Manager Style Performance,” found similar results. T. Daniel Coggin and Charles Trzcinka studied the performance of 292 pension plans with 12 quarters of data up to the second quarter of 1993. Here are their key findings:

• It is very difficult to find investment managers who consistently add value relative to appropriate benchmarks.

• There was no correlation found between relative performance in one period and future periods.

• There was no evidence the number of managers beating their benchmarks was greater than pure chance.

The authors concluded: “Those relying on historical data on returns are likely to be disappointed.”

It is evidence such as this that led Charles Ellis to declare active investing a loser’s game, one that is possible to win but the odds of doing so are so poor it isn’t prudent to try. Similarly, it would be imprudent for you to try to succeed if institutional investors, with far greater resources than you (or your broker or financial advisor), fail with great persistence. Remember, Ennis found that over the horizon of a decade, their likelihood of success was about 2%. The only reason for you to try would be if you could identify a strategic advantage that you had over these institutional players. The questions you might ask yourself are: Do I have more resources than they do? Do I have more time to spend finding future winners than they do? Am I smarter than all of these institutional investors and the advisors they hire? Unless when you look in the mirror you see Warren Buffet staring back at you, it doesn’t seem likely that the answer to any of these questions is yes. At least it won’t be yes if you are honest with yourself.

Investor Takeaways

Wall Street needs and wants you to play the game of active investing. They know that your odds of success are so low that it is not in your interest to play. But they need you to play so that they (not you) make the most money.

The financial media also want and need you to play so that you “tune in.” Again, that is how they (not you) make money. However, you have the choice of not playing the game of active management. You can simply earn market (not average) rates of return with low expenses and high tax efficiency. You can do so by investing in low cost, index funds, and other funds that are systematic and transparent in implementing their investment strategies. By doing so, you are virtually guaranteed to outperform the vast majority of both professionals and individual investors. In other words, you win by not playing. This is why active investing is called the loser’s game. It is not that the people playing are losers. And it is not that you cannot win. Instead, it is that the odds of success are so low that it is imprudent to try.

The only logical reason to play the game of active investing is that you place a high entertainment value on the effort. For some people there might even be another reason—they enjoy the bragging rights if they win. Of course, you rarely, if ever, hear when they lose.

It’s true that active investing can be exciting. Investing, however, was never meant to be exciting. Wall Street and the media created that myth. Instead, it is meant to be about providing you with the greatest odds of achieving your financial and life goals with the least amount of risk. That is what differentiates investing from speculating (gambling).

Many people get excitement from gambling on sporting events, horse races, or at the casino tables in Las Vegas. Prudent individuals, however, get entertainment value from gambling by betting only an infinitesimal fraction of their net worth on sporting events, etc. Similarly, even if you receive entertainment value from the pursuit of the “Holy Grail of Outperformance,” you should not gamble more than a tiny fraction of the assets on which you wish to retire (or leave to your children or favorite charity) on active managers being able to overcome such great odds.

Larry, I saw your post on alpha architect regarding "relative sentiment" factor. That factor research suggests institutions beat retail over the long term. But according to the data here institutions slightly underperform retail over previous 10 years. Does that mean it's a likely temporary underperformance of institutions versus retail or is relative sentiment not robust?

I knew active was suboptimal, didn’t realize it also applies to institutional investors as well!