Tariffs, Recession, and Downside Risk in Private Debt

Global equities fell sharply in response to the economic uncertainty and increased risk of recession created by the introduction of President Trump’s tariff policies. The decline, coupled with unprecedented volatility, could presage an economic slowdown or recession. Given that the risk of recession is a negative for private debt—credit spreads widen due to the potential for higher losses from future defaults, I thought it important to examine how an average recession would be expected to impact private credit. Before doing so, I’ll do a quick review of the performance of the two private credit interval funds, which provide limited quarterly liquidity (5%), in which I invest in order to gain exposure to the asset class: Cliffwater’s Corporate Lending Fund (CCLFX) which invests almost exclusively in senior, secured, floating rate private loans to borrowers backed by private equity sponsors, and their Cliffwater Enhanced Lending Fund (CELFX) that while investing in private loans, the majority of its allocation is in asset-backed strategies which are repaid by contractual cash flows from diversified pools of assets including less macro-correlated exposures in litigation finance, royalties, etc. Their corporate lending focuses primarily on businesses in sectors with less cyclical demand such as financials, health care, and information technology.

Performance Review

From inception in June 2019 through March 2025, CCLFX returned 9.64% with a standard deviation (SD) of just 1.81%. In comparison, broadly syndicated loans (BSL), as represented by the Morningstar LSTA US Leveraged Loan Index returned 5.63% with an SD of 6.61%, and one-month Treasury bills returned 2.52% with an SD of 0.64%. From its inception in July 2012, CELFX returned 12.75% with an SD of 1.12%, outperforming the BSL return of 6.22% (SD 3.49%) and the one-month Treasury bills return of 3.46% (SD 0.63%).

CELFX’s performance was even more impressive in the months when stocks and/or bonds provided negative returns.

· The average monthly loss for the S&P 500 when its return was negative was 4.15%. During these months the Bloomberg Aggregate Bond Index fell 1.59%. CELFX provided a positive return of 1.02%.

· During the months when the Bloomberg Aggregate Bond Index’s return was negative, the average loss was 1.59%. During these months the S&P 500 provided a negative return of -0.94% while CELFX returned +1.00%.

CCLFX returns during negative months for stocks and bonds were similarly impressive.

It’s important to add that while the two funds provide quarterly liquidity, the funds publish a daily net asset value (NAV), incorporating valuation changes of private loans (which are provided by lenders on a quarterly or monthly basis) as well reflecting volatility and price activity in the public BSL market where there is modest sensitivity of private loan valuations to that of the Morningstar LSTA US Leveraged Index of liquid loans. Thus, when credit spreads widen (or fall) in the public markets, or yields rise (or fall) both CCLFX and CELFX will make an adjustment to the valuation of its loans.

Recession Risks

Recession impacts private debt performance in two ways:

· Markdowns in loan values, in anticipation of future loan defaults, produce unrealized losses reflecting forecasts of future default losses by independent valuation firms. While they impact short-term performance they are reversed, typically over the next one to three years, and replaced by irreversible realized losses from defaults. Historically, valuation firms have tended to overestimate default losses which are subsequently rectified by higher reversals in unrealized losses.

· Loan defaults which permanently impair loan principal and interest.

The average recession has resulted in a GDP loss of about 2% and lasted about one year. Based on the historical evidence, Cliffwater estimated that the Cliffwater Direct Lending Index would produce returns of -0.5%, 13.5%, and 11.0% in 2025, 2026, and 2027, respectively. BDCs and drawdown funds (assuming leverage of 1:1) could expect after-fee returns equal to -9.0%, 17.5%, and 11.9% in 2025, 2026, and 2027, respectively. Three-year annualized recession-scenario expected returns are 7.8% for the CDLI and 6.2% for BDCs and drawdown funds.

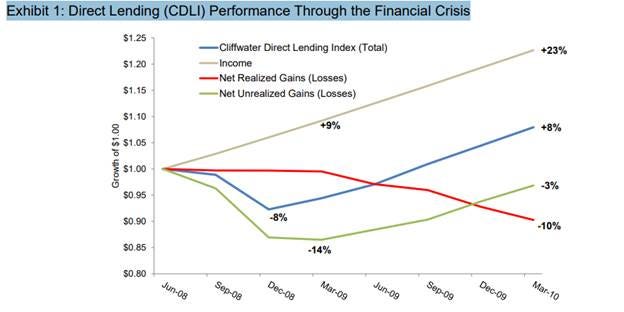

Cliffwater also examined what the performance of private credit was during the Great Financial Crisis.

The Global Financial Crisis (GFC)

The worst post-war recession occurred during the GFC. The exhibit below displays unlevered private debt performance from 2008 to 2010, represented by the CDLI, comprised equally between senior and second lien loans at the time. Per Cliffwater’s research, “The maximum downside for unlevered private debt (CDLI) was -8% (blue line) during the GFC, with interest income partially offsetting unrealized losses from loan markdowns. Exhibit 1 also reflects early markdowns in loan prices being reversed in later quarters as defaults produced realized losses totaling 10%. Levered private debt accounts saw a maximum downside of -16%, net of fees, during the GFC.”

Summarizing, while all crystal balls are cloudy, and recessions and their severity are impossible to predict, past data does provide useful evidence to understand the potential performance consequences for private debt. Without leverage, the evidence suggests that the impact of a typical recession on private, conservatively managed, credit is likely to be short-lived, modest, and well below those of equity and high yield debt. Leveraged accounts would not perform as well, however, and their drawdowns in the first year could exceed 10%. Of course, losses would be larger should a more severe, longer lasting recession occur.

Investor Takeaways

Investors who can accept the limited liquidity of the interval fund structure can benefit from the diversification benefits (low correlation to both stocks and bonds) of private credit funds such as CCLFX and CELFX, their resilience during economic downturns, and the illiquidity premium they provide. While they both provide equity-like expected returns (CCLFX’s average yield to maturity is 10.2% and CELFX’s current distribution rate is 11.0%), their volatility and downside risks have historically been a small fraction of both high-yield bonds and equities. Those characteristics make them a valuable addition to diversified portfolios.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future. He is also a consultant to RIAs as an educator on investment strategies.